KPMG and REC, UK Report on Jobs

Candidate availability expands at quickest rate for two-and-a-half years

Candidate availability expands at quickest rate for two-and-a-half years

Key findings

Candidate supply rises sharply amid hiring slowdown

Permanent placements fall, temp billings growth remains mild

Pay pressures moderate to 26-month low

Data collected June 12-26

Summary

The latest KPMG and REC, UK Report on Jobs survey, compiled by S&P Global, highlighted that lingering uncertainty over the economic outlook continued to weigh on hiring decisions at the end of the second quarter. Permanent placements fell solidly, while growth of temp billings remained mild overall. Total vacancies meanwhile expanded at the slowest pace in 28 months.

The slowdown in recruitment activity and reports of redundancies drove a steep and accelerated rise in overall candidate availability. Notably, the supply of both permanent and temporary workers increased at the sharpest rates since December 2020. At the same time, pay pressures remained marked but showed signs of cooling, with rates of both starting salary and temp wage inflation softening to their weakest in over two years in June.

The report is compiled by S&P Global from responses to questionnaires sent to a panel of around 400 UK recruitment and employment consultancies.

Staff recruitment held back by lingering uncertainty over the outlook

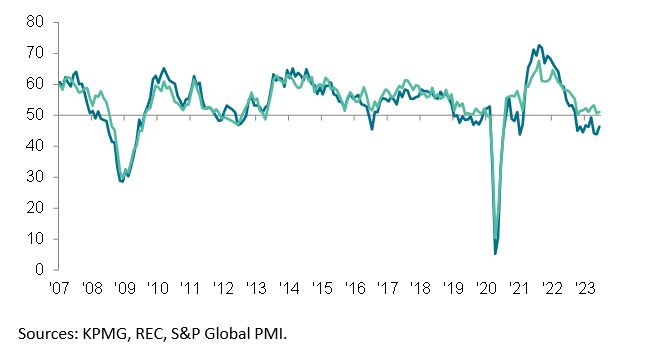

Recruitment consultancies indicated that companies continued to hesitate to take on additional staff in June, as uncertainty over the economic outlook weighed on hiring decisions across the UK. The latest survey data pointed to a solid fall in permanent staff appointments in June, albeit with the pace of contraction easing from May's near two-and-a-half-year record. At the same time, temp billings growth picked up slightly from May's recent low but remained mild overall.

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia

Save, Curate and Share

Save what resonates, curate a library of information, and share content with your network of contacts.

Permanent Placements Index

Temporary Billings

50.0 = no-change

Candidate supply rises rapidly in June

The hiring slowdown and company layoffs impacted staff availability, which rose for the fourth straight month in June. Moreover, the latest upturn in overall candidate numbers was the sharpest recorded since December 2020, with both permanent and temporary staff supply expanding at accelerated rates.

Starting pay increases at softest rate since April 2021

Latest data revealed further marked increases in both starting salaries and temp pay at the end of the second quarter. Panel members frequently mentioned that the rising cost of living and competition for skilled staff had pushed up starting salaries and temp wages. That said, remuneration for both permanent and temporary staff rose at the slowest rates for over two years in June.

Continued…

Vacancy growth eases to 28-month low

Overall vacancies continued to rise in June, but the pace of expansion softened for the fourth month in a row. Furthermore, the rate of growth was the softest recorded since the current sequence of rising staff demand began in March 2021. Underlying data indicated that a slower uptick in permanent vacancies offset a quicker rise in demand for short-term staff.

Regional and Sector Variations

Permanent placements fell across all four monitored English regions bar the North of England in June, which registered the first upturn since February.

London saw the steepest increase in temp billings of all four monitored English areas. The North was the only region to register a decline.

Demand for workers continued to rise across both the private and public sectors at the end of the second quarter. Stronger rates of vacancy growth were seen across the board compared to May, with the exception of permanent roles in the private sector. Notably, the latter saw the softest rate of expansion since February 2021. Meanwhile, the strongest rise in demand was signalled for permanent public sector staff.

Permanent staff vacancies expanded in eight of the ten job categories monitored by the survey in June. The steepest increases in demand were seen for Hotel & Catering and Blue Collar. Job openings meanwhile fell in the IT & Computing and Retail sectors.

The majority of monitored sectors recorded greater demand for temp workers during June, led by Hotel & Catering by a wide margin. IT & Computing and Construction were the only job categories to register lower vacancies for short-term workers.

Comments

Commenting on the latest survey results, Claire Warnes, Partner, Skills and Productivity at KPMG UK, said:

“The sharp upturn in candidate availability this month – the highest for two and a half years – is a big concern for the economy reflecting the effects of a sustained slowdown in recruitment along with increasing redundancies across many sectors.

“Employers are also tending towards temporary hires, given lingering economic uncertainty. And yet, the labour market remains reasonably resilient, with notable demand for skilled workers, both permanent and temporary, across a multitude of sectors this month.

“The evident mismatch between open vacancies and the skills of available candidates needs to be addressed urgently and a concerted focus on upskilling and reskilling is long overdue.”

Neil Carberry, REC Chief Executive, said:

“There is a risk of seeing an element of Groundhog Day in June hiring, with permanent billing easing again and firms still turning to temporary staff in the face of uncertainty. But there was quite a lot of change in the shadows of the headline data. There was a significant step up in the number of candidates looking for a new permanent or temporary role. This is likely driven by people reacting to high inflation by stepping up their job search, and by some firms reshaping their businesses in a period of low growth. It’s no surprise, therefore that the rate at which wages are rising has dropped again.

“Despite these trends, the labour market remains very tight. There are still broad skills shortages, with accountancy, construction, teaching and nursing among those sectors struggling to find and retain workers. This is despite the supply of candidates across the job market having risen for four consecutive months. Earlier this month, the government published its first ever NHS Workforce Plan, which acknowledges significant staffing issues while not getting to grips with the NHS being really bad at building partnerships with staffing partners such as agencies.

“The growth in vacancies for temps and permanent staff in hotel & catering and blue-collar jobs, and for temp positions in retail, suggest businesses anticipate that people are still prepared to spend their wages on goods and services despite the fall in their purchasing power and the wider cost-of-living crisis. This is backed by anecdotes from REC members noting that the warm weather in June was a significant driver of demand.

“Long-term progress rests on the UK being a great place to invest. A strong industrial strategy with people at its heart would help overcome labour and skills shortages, acknowledging the wide range of choices that people have about how they work. Progress should start with action on skills and immigration, but also accelerating steps on childcare, transport and back-to-work support, as set out in the REC’s Overcoming Shortages report.”

Contact

S&P Global

Annabel Fiddes

Economics Associate Director

S&P Global Market Intelligence

T: +44 (0)1491 461 010

Sabrina Mayeen

Corporate Communications

S&P Global Market Intelligence

T: +44 (0) 7967 447030

Methodology

The KPMG and REC, UK Report on Jobs is compiled by S&P Global from responses to questionnaires sent to a panel of around 400 UK recruitment and employment consultancies.

Survey responses are collected in the second half of each month and indicate the direction of change compared to the previous month. A diffusion index is calculated for each survey variable. The index is the sum of the percentage of ‘higher’ responses and half the percentage of ‘unchanged’ responses. The indices vary between 0 and 100, with a reading above 50 indicating an overall increase compared to the previous month, and below 50 an overall decrease. The indices are then seasonally adjusted.

Underlying survey data are not revised after publication, but seasonal adjustment factors may be revised from time to time as appropriate which will affect the seasonally adjusted data series.

For further information on the survey methodology, please contact economics@hismarkit.com.

Full reports and historical data from the KPMG and REC, UK Report on Jobs are available by subscription. Please contact economics@hismarkit.com.

June 2023 Update

In June 2023, new seasonally adjusted retail vacancies (permanent and temporary) numbers were added to the REC/KPMG Report on Jobs datasets.

Please note the new retail data have also been weighted into the respective indices for aggregate vacancies (permanent, temporary and total). All vacancies data will have a fixed back history from June 2023.

About KPMG

KPMG LLP, a UK limited liability partnership, operates from 22 offices across the UK with approximately 15,300 partners and staff. The UK firm recorded a revenue of £2.43 billion in the year ended 30 September 2021.

KPMG is a global organization of independent professional services firms providing Audit, Legal, Tax and Advisory services. It operates in 145 countries and territories with more than 236,000 partners and employees working in member firms around the world. Each KPMG firm is a legally distinct and separate entity and describes itself as such. KPMG International Limited is a private English company limited by guarantee. KPMG International Limited and its related entities do not provide services to clients.

About REC

The REC is the voice of the recruitment industry, speaking up for great recruiters. We drive standards and empower recruitment businesses to build better futures for their candidates and themselves. We are champions of an industry which is fundamental to the strength of the UK economy. Find out more about the Recruitment & Employment Confederation at www.rec.uk.com.

About S&P Global

S&P Global (NYSE: SPGI) S&P Global provides essential intelligence. We enable governments, businesses and individuals with the right data, expertise and connected technology so that they can make decisions with conviction. From helping our customers assess new investments to guiding them through ESG and energy transition across supply chains, we unlock new opportunities, solve challenges and accelerate progress for the world.

We are widely sought after by many of the world’s leading organizations to provide credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity and automotive markets. With every one of our offerings, we help the world’s leading organizations plan for tomorrow, today. www.spglobal.com.

Disclaimer

The intellectual property rights to the data provided herein are owned by or licensed to S&P Global and/or its affiliates. Any unauthorised use, including but not limited to copying, distributing, transmitting or otherwise of any data appearing is not permitted without S&P Global’s prior consent. S&P Global shall not have any liability, duty or obligation for or relating to the content or information (“data”) contained herein, any errors, inaccuracies, omissions or delays in the data, or for any actions taken in reliance thereon. In no event shall S&P Global be liable for any special, incidental, or consequential damages, arising out of the use of the data.

This Content was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global. Reproduction of any information, data or material, including ratings (“Content”) in any form is prohibited except with the prior written permission of the relevant party. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content.