LSIs: Fast becoming significant

LSIs: Fast becoming significant

National approaches to the supervision of less significant institutions (LSIs) have remained uneven during the SSM’s first two years. While retaining its focus on proportionality, the ECB is pushing for more harmonized supervision of significant and less significant institutions. This is a fast evolving area, pushed and further complicated by Brexit. LSIs need to be aware of the potential effects of this supervisory convergence and factor them into their strategic planning.

Why is the ECB increasing its focus on LSIs?

Since the SSM’s inception, the ECB’s primary focus has been on direct supervision of the 125 Significant Institutions (SIs) that represent about 80% of Eurozone banking assets. National Competent Authorities (NCAs) have continued to supervise the remaining 3,244 Less Significant Institutions (LSIs) under ECB oversight.

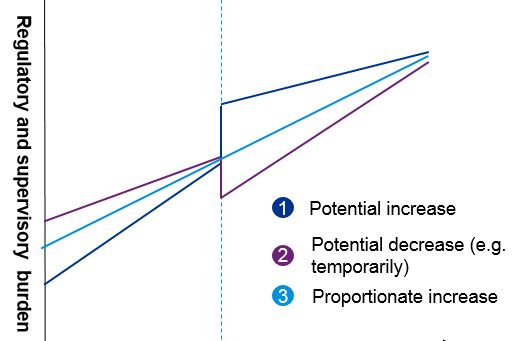

After two years, and with Brexit on the horizon, this approach is showing its shortcomings. While the ECB has had some success in harmonizing SI supervision, the treatment of LSIs has continued to differ between Member States. This means that LSIs in different countries can experience very different transitions to SI status (see Figure 1).

Figure 1: Potential effects of the transition from LSI to SI supervisionpotential-effects

In response, the ECB is increasing its focus on LSIs. The goal is to ensure harmonized supervision and prevent regulatory arbitrage between LSIs and SIs.

The resulting changes have greatest significance for LSIs that have recently met, or will soon meet, the criteria for SI status. LSIs with a ‘High Priority’ ranking could also move closer to the SI supervisory model. Brexit could give the changes even greater impact, as some LSIs build up their activities within the Single Market on the continent.

What is the impact of transition from LSI to SI?

For most banks, the transition from LSI to SI status takes about two years. It begins when an LSI triggers one of five criteria relating to size, economic importance, cross-border activities, ESM assistance or national ‘Top 3’ status. Once informed of this by an NCA, the ECB carries out a Comprehensive Assessment and confirms the bank’s supervisory status. A new SI then has a few months to prepare for direct ECB supervision.

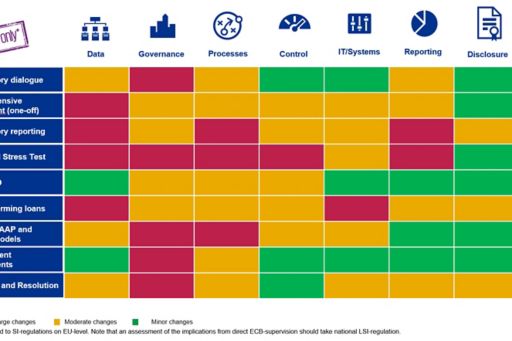

Moving from LSI to SI status has a complex and significant impact on a bank’s supervisory burden (see Figure 2). The most important areas of change can be summarized under six headings.

- Greater formalization. Direct supervision by the ECB involves more formality over areas including mixed Joint Supervisory Teams, On-Site Inspections, Thematic Reviews and Reviews of Internal Models.

- The Comprehensive Assessment (CA). Before entering direct ECB supervision LSIs undergo a three-stage CA, comprising a Supervisory Risk Assessment, an Asset Quality Review and a full Stress Test.

- Additional reporting. SI status carries additional reporting requirements in a number of areas including FINREP, COREP, Non-Performing Loans (NPLs) and Statistical Reporting.

- Capital Requirements. The Supervisory Review and Evaluation Process (SREP) and a comprehensive Stress Test are core components of Pillar 2 capital calculations for SIs.

- Governance and Risk Management. In recent years the ECB has set more specific expectations for SI governance and risk management, including ICAAP, ILAAP, risk appetite and NPLs. It is also expected to set out new expectations for outsourcing.

- CRR and CRD. The ECB takes its own approach to the various options and discretions applicable to CRR/CRD, which can differ from the approach taken by individual NCAs.

Figure 2: From LSI to SI – an indicative ‘heat map’ of supervisory changes

Can the ECB reconcile harmonization with proportionality?

The SSM Regulations not only call for supervisory harmonization. They also require the ECB to take a proportionate approach to direct supervision and the guidance it issues to NCAs. For SIs, this is usually achieved by providing common standards and expectations, which are applied on a bank-by-bank basis by Joint Supervisory Teams. For LSIs, the ECB takes measures to ensure proportional supervision in four areas:

- Prioritization: Categorizing LSIs as Low, Medium or High Priority each year.

- Standards: Ensuring that NCAs are applying consistent, appropriate policies of LSI supervision.

- Assessment: Assessing risky, complex LSIs more stringently and vice versa.

- Reporting: Tailoring the frequency and detail of LSIs’ notification and reporting requirements.

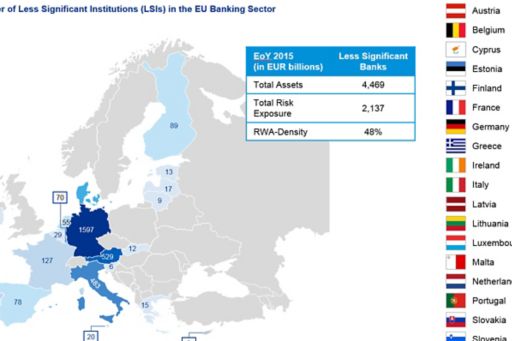

Even so, there is inevitable tension between the goals of proportionality and harmonization. Although LSI and SI supervision are converging in some countries, the reality is that different NCAs still apply proportionality in different ways. This reflects wide variation in the number, size and concentration of credit institutions in different Member States (see Figure 3). Flexibility in guidance notes issued to NCAs by the ECB’s Directorate-General for Micro-Prudential Supervision is a factor too. But local supervisory or political priorities can also encourage NCAs to take different approaches to comparable institutions.

Figure 3: Overview of LSIs in the Euro area, end of 2015

In response to these persistent differences, the ECB took a number of steps to harmonize the supervision of SIs and LSIs during 2016. These included:

- Completing Joint Supervisory Standards (JSSs) on supervisory planning and recovery planning;

- Developing JSSs for on-site LSI inspections and the supervision of car finance institutions;

- Establishing a crisis management framework for co-operation between the ECB and NCAs; and

- Making further progress on a common SREP methodology for LSIs.

Looking ahead: LSIs need to be prepared

We expect the ECB to further increase its focus on LSIs over the coming year. Individual banks need to factor the differences between LSI and SI supervision - and between different NCAs’ approaches to LSIs - into their strategic planning. They should also consider possible complications arising from Brexit. These could include the supervisory effect of moving operations from the UK to the EU-27, and the potential impact of the proposed EU Intermediate Holding Company rules.

LSIs should be in no doubt that the ECB’s work in this area could have a significant impact on their supervisory burden, and even on the viability of their wider business models.