SREP 2016 vs SREP 2017

SREP 2016 vs SREP 2017

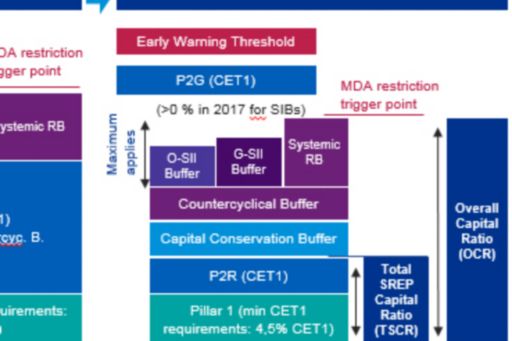

How do the quantitative results of the SREP decision differ in construction from last year.

The 2017 quantitative results of the SREP decision differ in construction from last year (2016). Some banks have reported that the wording in the letters can be confusing; and banks are now subject to the Total SREP Capital Requirement (TSCR) and an Overall Capital Requirement (OCR).

According to the SREP Benchmark study conducted by KPMG’s ECB Office in October 2016, the sample median for P2R is 225 bps, while P2G is 200 bps. Sample data indicates that a worse score from the supervisory review tends to result in a higher P2R. However, correlations of P2R with bank type and total assets generally tend to be weak. Mainly the CET1 requirements excluding P2G is lower when compared to SREP 2015, consequently the MDA trigger is lower since P2G is not MDA relevant.

The 2016 stress test results should be reflected in P2G, however several additional factors are also likely to have been considered by JSTs when setting P2G (since there is no direct translation of stress test results in P2G). In addition, data suggest a minimum of 100 BP for P2G. Including P2G, the CET1 demand is somewhat higher compared to 2015.

The publication of the results remains uncertain. The ECB does not dissuade institutions to disclose MDA-relevant capital requirements and highlights that P2G is not MDA relevant. With regard to P2R, some banks have indeed disclosed it; but, P2G has not been disclosed so far.

A harmonized SREP process is an important step towards achieving a level playing field in European banking. If we consider our experience from the recent years, 2015 was the year when the pan-European SREP was applied for the first time, with the stress test taking place in 2016. What’s next? We have seen a great deal of progress in the area of harmonization over the course of 2016, and we expect that this will likely inform SREP 2017. Factors include:

- The EBA’s publication of the public consultation on the Guidelines on ICT Risk Assessment under the SREP process may affect, for instance, the assessment of Business Model, Corporate Governance and Operational Risk.

- The develop and fine tuning of a best practice approach addressing specific IT risks and guidance on cyber risk may have relevant impact as well final valuation of the banks.

- Publication of the EBA’s final Report on Draft Guidelines on ICAAP and ILAAP information collected for SREP purposes is another aspect contributing to changes regarding the governance of the ICAAP/ILAAP, the identification of risk categories and subcategories, and some other changes in ILAAP and stress test. As ICAAP and ILAAP procedures are still quite un-harmonized in the different countries of the Eurozone, it wouldn’t be a surprise if more challenge, guidance and best practices are recommended by the ECB over the course of the next year.

- The EBA´s public consultation on the Draft guidelines on internal governance may affect and influence Corporate Governance assessment.

- The ECB’s draft guide on the treatment of NPLs raises not only questions regarding the level of NPLs (i.e. informing SREP’s Business model assessment and the risks to capital) but also Governance issues, like NPL strategies, separation of responsibilities or separate NPL desks.

- With respect to credit risk, the ECB’s expectations regarding Leveraged Finance will play a role in future years’ SREPs too.

- The European Commission has published a comprehensive package of reforms to the capital requirements (CRR/CRD IV) and resolution framework (BRRD/SRM) amendments that may shed some light on the MREL-P2G-P2R joint impact, although this proposal is still at the beginning of a long legislative process.

Taking all this together, even if one expects the structure of the capital requirements to have reached a mature shape and form, as it pertains to content, the ECB, the EBA and the EU Commission are still progressing with harmonization. More updates to the standards that the ECB uses to check compliance and appropriateness are expected.