MREL – Impact on funding and business strategy still unknown

MREL – Impact on funding and business strategy

MREL adds another layer of uncertainty for banks.

The Banking Recovery and Resolution Directive (BRRD) which entered effect on 1 January 2016 sets out the EU approach to avoiding the bailout of banks with public money. This is achieved by requiring banks to have a funding structure with a certain proportion of liabilities that can be written off or converted into equity in the event of a bank failure (that is: “bailed-in”). Such liabilities, in combination with equity, are known as MREL (Minimum Requirement for Own Funds and Eligible Liabilities). The MREL-requirements and criteria within the BRRD have recently been elaborated further by the EBA in the final version of a Regulatory Technical Standard.

MREL target levels will be set at group and solo level on a case-by-case basis, however, in 2016, focus is given to requirements for consolidated banking groups, whereas requirements for subsidiaries will be specified in a second stage, taking the consolidated requirement into account. Future target levels will be subject to annual review by the Single Resolution Board (SRB). While it may seem fitting for bail-in to be set on a case-by-case basis, it may also be easy to understand why banks may feel uncertainties around MREL.

Banks facing multiple uncertainties on MREL

For banks, the political dimension of the European bail-in regime adds to other sources of uncertainty when it comes to the implementation of MREL and their funding plans:

Priority of liabilities: Although addressed by a current consultation , the insolvency creditor hierarchies still differ between EU members which could hinder the use of the bail-in tool. Therefore the EU commission aims to establish a standardized approach to creditor ranking in insolvency and is likely to seek a compromise between a French approach, which includes the creation of sub-senior bonds, and a German model which subordinates plain-vanilla senior unsecured debt to deposits, derivatives and structured notes.

Pricing: Market participants currently have to factor in changes in the priority of bail-in liabilities in creditor hierarchy, and the (as yet unknown) MREL targets to be set by the SRB individually for each bank. These factors increase the potential volatility of future profitability. At an industry meeting in January 2016, the SRB did not favor a public disclosure of the MREL target level, although it recognized the importance for investors of obtaining the information necessary to assess and price the risk of investing in the debt instruments of institutions efficiently. However, in July the SRB announced that it is within the discretion of banks to disclose the MREL target levels, similar to the ECB allowing (but not obliging) banks to disclose their 2015 Pillar 2 requirements.

Collateral eligibility: According to Article 64 of the ECB guidelines on eligibility debt instruments that are subordinated to other debt instruments issued by the same issuer are excluded. This may limit refinancing options for European banks holding debt instruments with different seniorities.

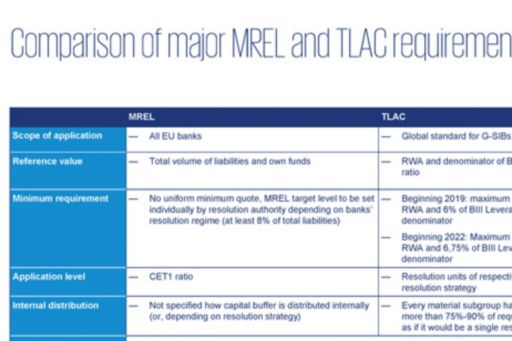

Alignment with Total Loss Absorbing Capacity (TLAC) requirements: TLAC represents an additional regulatory requirement that will enter into force on 1st of January 2019. In contrast to MREL (a ‘Pillar 2’ measure set individually by the SRB for each bank), TLAC requires a minimum amount of loss absorbing capacity for G-SIBs in relation to their risk-weighted assets (RWAs) and the denominator of the Basel III Leverage Ratio (see table 1 for a comparison of MREL and TLAC standards). The EU commission intends to make a proposal to introduce this standard into EU law in 2016 and considers three different options, favouring an integrated approach where TLAC-liabilities are integrated into CRR-requirements for Tier 2 capital, i.e. an increase in Pillar 1 requirements. The EBA in its interim report on the implementation and design of the MREL framework recommends harmonising the reference base for the MREL requirement with FSB’s TLAC standard and changing the denominator to RWAs instead of total liabilities incl. own funds. Furthermore TLAC uses the concept of internal TLAC for material sub-groups, however, to date the BRRD does not distinguish between internal and external MREL. Consequently further changes of EU law to transpose the internal TLAC requirements of the FSB appears likely that might also affect the corporate structure of major banks.

Close monitoring of MREL-specification necessary

Summarizing these ongoing debates, banks and investors currently face considerable uncertainties with regard to MREL-implementation and its impact on banks’ funding, profitability and corporate structure. They know the contours of how the G20 ‘bail-in’ principles will be implemented in Europe. But they await key clarifications for this major element of the European resolution regime, to enable banks to design their responses and investors to understand the final impact.