e-Tax alert 102 eng- E-services income tax regime

e-Tax alert 102 eng- E-services income tax regime

Following the implementation of the VAT regime on e-services provided by foreign e-services providers in 2016, the Ministry of Finance has recently promulgated the relevant income tax regime. Similar to the VAT regime, the income tax regime focuses on the revenue received by foreign e-services providers from their e-services provided to onshore Taiwan customers.

Following the implementation of the VAT regime on e-services provided by foreign e-services providers in 2016, the Ministry of Finance has recently promulgated the relevant income tax regime. Similar to the VAT regime, the income tax regime focuses on the revenue received by foreign e-services providers from their e-services provided to onshore Taiwan customers.

The main points of the income tax regime are as follows:

1. What types of transactions are addressed under the Income tax regime?

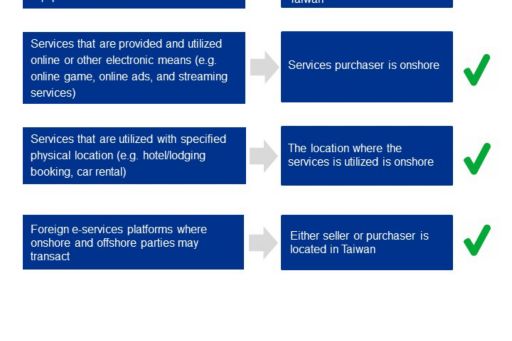

Similar to the VAT regime, the following types of activities are addressed under the income tax regime as well: “Sale of e-services” and “Services that are utilized with specified physical location within Taiwan”.

For “sale of e-services”, it refers to either: services that are provided and utilized through internet download or other electronic transmission to computer equipment or mobile devices, or services that are provided and utilized online or other electronic means (e.g. online game, online ads, and streaming services).

While “services that are utilized with specified physical location within Taiwan” refers to: services that are provided through the internet or via other electronic means and utilized at a physical place such as hotel/lodging booking , car rental services.

2. The determination and calculation of Taiwan sourced income

In accordance with the Taiwan income tax rule, foreign entities would only be subject to Taiwan income tax on income derived that are Taiwan sourced.

Under the context of the income tax regime on e-services, the following types of income are considered as Taiwan sourced:

a. For “sale of e-services” type of transaction, income derived from services that are provided entirely offshore but requires onshore individual or enterprise's assistance to complete the provision.

b. For ”services that are utilized with specified physical location within Taiwan”: if the location where the services is utilized is onshore.

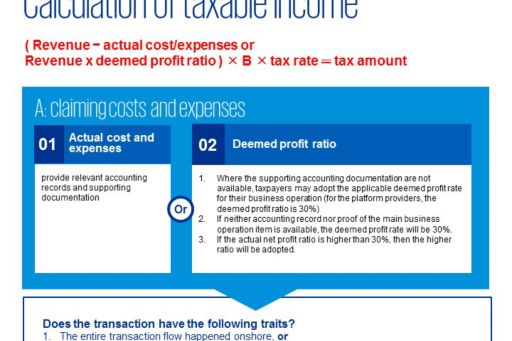

In terms of the calculation of the taxable income, the income tax regime allows the foreign e-services providers to claim actual costs and expenses incurred or adopt a deemed profit ratio. However, the use of deemed profit ratio would require pre-approval from the authority.

In addition, the tax regime also allows the taxpayers to claim a contribution ratio, which determines how much of revenue derived is attributable to onshore activities and offshore activities. Similar to the utilization of deemed profit ratio, the use of contribution ratio would also require pre-approval from the tax authority.

3.When will the income tax regime become effective and what period will be covered?

The income tax regime would be effective starting from January 1st, 2017, and the first self-reporting would need to be made during the month of May 2018 and before May 31st, 2018.

For your ease of understanding, an illustration of the flow of the income tax regime is illustrated below.

KPMG Observation

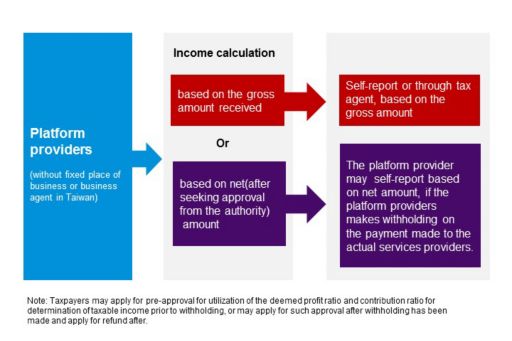

1. If foreign e-service providers (including both platform providers and non-platform providers) wishes to adopt deemed profit ratio and contribution ratio in the calculation of their taxable income, pre-approval from the tax authority would be required.

2. While platform providers may apply with the tax authority and be subject to withholding based on the net amount of the payment they received, e.g. the relevant transaction/services fee which they charge to the actual e-service providers, however, under such scenario the platform providers would need to make withholding on the portion of the payment (received from the Taiwan services purchasers) which they pay to the actual e-services providers, and pay the withholding tax amount collected to the tax authority.

3. The utilization of the deemed profit ratio and contribution ratio will only be applied to income received starting from 2017. Nonetheless, for income received prior to and including 2016, the foreign e-service may still claim actual costs and expenses incurred.

4. Foreign e-service providers may apply for refund of any excess tax payment arising under the implementation of the e-service income tax regime, within 5 years after the date with the payment is received.

Lynn Chen

Partner, Tax department

e-Tax alert

© 2024 KPMG, a Taiwan partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved.

For more detail about the structure of the KPMG global organization please visit https://kpmg.com/governance.

上列組織及本文內任何文字不應被解讀或視為上列組織之間有任何母子公司關係,仲介關係,合夥關係,或合營關係。 上述成員機構皆無權限(無論係實際權限,表面權限,默示權限,或任何其他種類之權限)以任何形式約束或使得 KPMG International 或任何上述之成員機構負有任何法律義務。 關於此文內所有資訊皆屬一般通用之性質,且並無意影射任何特定個人或法人之情況。即使我們致力於即時提供精確之資訊,但不保證各位獲得此份資訊時內容準確無誤,亦不保證資訊能精準適用未來之情況。任何人皆不得在未獲得個案專業審視下所產出之專業建議前應用該資訊。