e-Tax alert 101 eng- Taiwan announced thresholds for MF and CBC reports submission

e-Tax alert 101 eng

Taiwan Ministry of Finance (MOF) announced amendments made to “Regulations Governing Assessment of Profit-Seeking Enterprise Income Tax on Non-Arm’s-Length Transfer Pricing” (“TP assessment Rules”) on November 13, 2017. Most of the amendments reflect the requirements listed under OECD BEPS Action 13 Report. Major amendments include multinational enterprises (MNE) who have members in Taiwan may be required to file Master File and Country-by-Country Report. This amendment will be applicable from fiscal years of 2017 onward.

Taiwan Ministry of Finance (MOF) announced amendments made to “Regulations Governing Assessment of Profit-Seeking Enterprise Income Tax on Non-Arm’s-Length Transfer Pricing” (“TP assessment Rules”) on November 13, 2017. Most of the amendments reflect the requirements listed under OECD BEPS Action 13 Report. Major amendments include multinational enterprises (MNE) who have members in Taiwan may be required to file Master File and Country-by-Country Report. This amendment will be applicable from fiscal years of 2017 onward.

In view of the compliance cost of MNEs for preparing transfer pricing documents, On December 11, 2017, MOF released Safe Harbor Rules for Master File and Country-by-Country Report in Taiwan after taking into accounts of international practices, national conditions in Taiwan and public opinions.

KPMG Observation

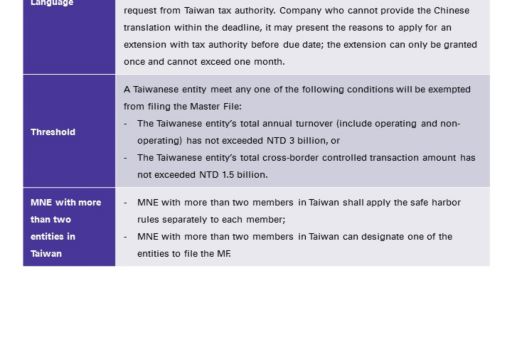

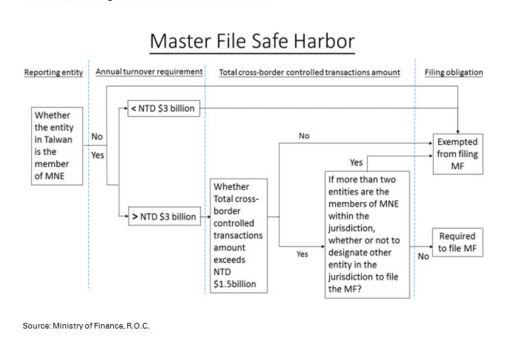

The safe harbor threshold for the preparation of master file is lower than those for CBCR. Hence, the Taiwanese entity of a MNE group should evaluate if it needs to prepare the MF. If yes, the MF needs to be ready when filing the income tax return and needs to be submitted with Taiwan tax authority within 12 months after the last day of the reporting fiscal year.

For foreign MNE groups, the MF is usually centrally prepared at headquarters’ level. We recommend Taiwanese subsidiaries/branches of a foreign MNE to inform their headquarters as early as possible to make sure the MF can be ready by filing deadline (e.g. end of May for calendar year taxpayer) and to obtain a copy of MF for submission.

As Taiwan also has transfer pricing documentation requirement, it is also suggested to double check if the content in the MF is consistent with the Taiwanese transfer pricing report.

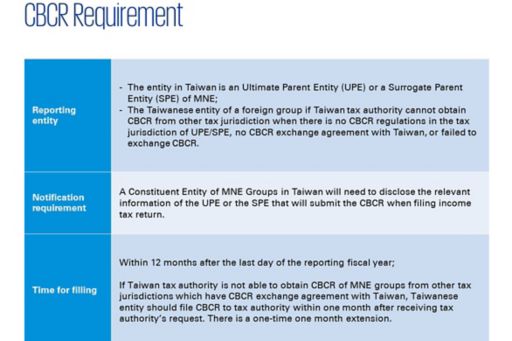

As for CBCR, if the revenue of a foreign MNE groups exceed the CBCR threshold of NTD 27 billion or if the entity do not qualify for the above thresholds, we recommend Taiwanese subsidiaries/branches of a foreign MNE to take the following actions:

- Ask the headquarters for the information of the CBCR filing entity (i.e. UPE or SPE);

- Disclose the information of UPE or SPE on the disclosure forms to be attached with tax return at time of filing; and

- If it is expected Taiwanese tax authority cannot obtain a copy of CBCR through tax information exchange mechanism, the Taiwanese entity should obtain a copy of the CBCR for submission.

KPMG BEPS Services Team

Ellen Ting

Partner, Tax department

e-Tax alert

© 2024 KPMG, a Taiwan partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved.

For more detail about the structure of the KPMG global organization please visit https://kpmg.com/governance.

上列組織及本文內任何文字不應被解讀或視為上列組織之間有任何母子公司關係,仲介關係,合夥關係,或合營關係。 上述成員機構皆無權限(無論係實際權限,表面權限,默示權限,或任何其他種類之權限)以任何形式約束或使得 KPMG International 或任何上述之成員機構負有任何法律義務。 關於此文內所有資訊皆屬一般通用之性質,且並無意影射任何特定個人或法人之情況。即使我們致力於即時提供精確之資訊,但不保證各位獲得此份資訊時內容準確無誤,亦不保證資訊能精準適用未來之情況。任何人皆不得在未獲得個案專業審視下所產出之專業建議前應用該資訊。