e-Tax alert 98 - Taiwan income tax reform impacts and observation

e-Tax alert 98 - Taiwan income tax reform impacts

In view of the complexity of the current imputation tax system, issues concerning the higher tax burden on dividends income faced by domestic shareholders and the tax burden difference between domestic and foreign investors, the Ministry of Finance (“MOF”) has proposed to reform the current Income Tax Act in order to simplify the tax system, to adjust the tax rate structure of individual income tax (“IIT”), corporate income tax (“CIT”), and the surtax on undistributed earnings (“Surtax”), and to ease the income tax burden on wage earners and mid and low-income earners. The draft bill has been raised to the Cabinet for approval on September 1st, 2017 and is expected to be submitted to the Legislature in mid-October.

In view of the complexity of the current imputation tax system, issues concerning the higher tax burden on dividends income faced by domestic shareholders and the tax burden difference between domestic and foreign investors, the Ministry of Finance (“MOF”) has proposed to reform the current Income Tax Act in order to simplify the tax system, to adjust the tax rate structure of individual income tax (“IIT”), corporate income tax (“CIT”), and the surtax on undistributed earnings (“Surtax”), and to ease the income tax burden on wage earners and mid and low-income earners. The draft bill has been raised to the Cabinet for approval on September 1st, 2017 and is expected to be submitted to the Legislature in mid-October. The key points of the tax reform are summarized below:

For the IIT treatment on dividend income for individual residents (i.e. the domestic individual investors)

- Abolish the imputation tax system

- Two alternative tax plans to tax the dividends:

- Plan A will allow individual investors to be exempt from income tax on 37% of dividends they receive, with the remaining 63% to be included in their IIT return and taxed accordingly.

- Plan B will allow the individual investors to choose between two options, whichever gives more favorable outcome: Option 1 will tax all dividend income as part of individual income, individual investor can recognize 8.5% of the dividend income as tax deductible amount, (up to NT$80,000 as the maximum allowable deduction amount for each household). Under Option 2, the dividend will be taxed separately and not included as part of the individual income, the individual investor will be taxed on a flat rate of 26 %, rather than the individual income tax rate.

For the withholding tax (“WHT”) treatment on dividend income for non-residents (i.e. the foreign investors)

- Surtax paid on undistributed earnings can no longer be used to offset against the WHT imposed on the dividend distributed to foreign investors.

- WHT rate on dividend income is increased from 20 % to 21 % for foreign investors.

For CIT

- The CIT rate is increased from 17 % to 20 %.

Companies will no longer be required to establish, record, calculate, and distribute of Imputation Credits Account (“ICA” account due to the abolishment of imputation tax system).

- The decrease of Surtax rate from 10 % to 5%.

- The tax transparent treatment on sole-proprietorship and partnership, i.e. the income will be subject to IIT at the sole proprietor and partner’s level.

- Dividend received by domestic corporate shareholder from their investment in other domestic companies, will likely to remain exempt from CIT.

For IIT

- The 45% tax rate bracket for net consolidated income over NTD 10 million will be abolished. The highest tax rate bracket will be restored to 40%.

- Upward adjustment of the following three deductions: Standard deduction will increase by NTD 20,000, raised from NTD 90,000 to NTD 110,000. The amount will be doubled for taxpayers with spouse. Special deduction for income from salaries / wages and special deduction for disabled and handicapped will increase by NTD 52,000, raised from NTD 128,000 to NTD 180,000, respectively.

The tax reform is anticipated to be a priority bill since the implementation dates planned are set as follows:

- Individual dividend income tax for domestic investors and individual income tax: Effective starting from January 1, 2018, i.e., applicable when filing FY 2018 individual income tax return in 2019.

- Dividend withholding tax for foreign investor: The raised withholding rate will take effect from January 1, 2018. Regarding the abolishment of creditable surtax, considering the levy of surtax is in the year subsequent to the CIT reporting, such new regime will take effect from January 1, 2019.

- Corporate Income Tax: The adjusted tax rate and new taxation regime for sole -proprietorship and partnership will be applicable upon filing FY 2018 corporate income tax return and surtax return. To work in conjunction with the new dividend income tax regime, the abolishment of imputation credit account will take effect from January 1, 2018.

KPMG Observation

Generally speaking, the proposed tax reform will reduce the tax burden for domestic investors on dividend income, reduce the individual income tax rate, and raising the foreign investor’s tax burden on dividend income so as to reduce the gap in tax treatments between local/foreign investors. Furthermore, the tax reform will also raise the corporate income tax rate, reduce the surtax rate, abolish the imputation tax credit system, implement new tax regime on sole-proprietorship and partnership which improve the structure on tax rates and tax calculation; raise individual income tax deduction amount for the benefit of wage earners and mid and low-income earners. Overall, the proposed tax reform is a big step forward for Taiwan’s tax system to become more aligned with international trend and practice.

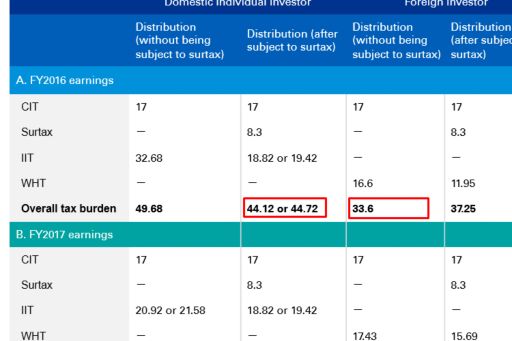

To illustrate the tax impacts of the proposed tax reform on local and foreign investors, using the following simulation, where FY 2016, FY 2017, and FY2018’s earnings of 100 dollars are distributed in FY 2017, FY 2018, and FY 2019 respectively (not subject to surtax), versus the scenario where the earnings are distributed in FY 2018, FY 2019, and FY 2020 respectively (having been subject to surtax). In the simulation, assuming in the case of domestic individual the applicable individual income tax rate is 45%:

Based on the above simulation, the following observations can be made with respect to the proposed tax reform:

- With respect to surtax impact on undistributed retained earnings, except for the case involving domestic corporation distributing its FY 2016 earnings to domestic individuals (since the new regime would applied if distribution is made after surtax has been imposed), in all other cases, the overall income tax burden would increase.

- For domestic individual investors, the overall income tax burden would become lower after the tax reform.

- For foreign investors, the overall income tax burden would become higher after the tax reform. However, in the case where the foreign investor’s resident country has entered in tax treaty with Taiwan, the potential reduced withholding tax rate on dividend can still be used. It should be noted, though, it is likely that starting from January 1, 2019, surtax previously paid in undistributed retained earnings may no longer be used to offset against the withholding tax imposed on the dividend distribution.

- For mid and low-income earners, they may opt for consolidated reporting regime to enjoy tax credit under the “Plan B” regime.

Authors

Kevin Chen

Partner, Tax department

Lynn Chen

Director, Tax department

Chuck Chiu

Associate Director, Tax department

e-Tax alert

© 2024 KPMG, a Taiwan partnership and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved.

For more detail about the structure of the KPMG global organization please visit https://kpmg.com/governance.

上列組織及本文內任何文字不應被解讀或視為上列組織之間有任何母子公司關係,仲介關係,合夥關係,或合營關係。 上述成員機構皆無權限(無論係實際權限,表面權限,默示權限,或任何其他種類之權限)以任何形式約束或使得 KPMG International 或任何上述之成員機構負有任何法律義務。 關於此文內所有資訊皆屬一般通用之性質,且並無意影射任何特定個人或法人之情況。即使我們致力於即時提供精確之資訊,但不保證各位獲得此份資訊時內容準確無誤,亦不保證資訊能精準適用未來之情況。任何人皆不得在未獲得個案專業審視下所產出之專業建議前應用該資訊。