"Arm's length" interest rates for 2018

"Arm's length" interest rates for 2018

Serbian Ministry of Finance has adopted the Rulebook on arm’s length interest rates for 2018

We would like to inform you that the Serbian Ministry of Finance (“MF”) has adopted the Rulebook on arm’s length interest rates for 2018 (“the Rulebook”). The Rulebook was published in the Official Gazette of Serbia No. 18/2018 dated 9 March 2018. The Rulebook contains the prescribed interest rates applicable to taxpayers who had or will have related party financing during 2018.

The Rulebook is effective as of 17 March 2018 and will be in force until 31 December 2018.

Impact of the Rulebook to transfer pricing documentation for 2018 and application of Double Tax Treaties

According to the provisions of Articles 59, 60 and 61 of the Corporate Income Tax Law (“the CIT Law”), in determining arm’s length interest expense/revenue, taxpayers can:

1. use interest rates as prescribed by the MF Rulebook or

2. apply general OECD based methods for assessment of arm’s length interest as prescribed by the CIT Law.

Taxpayers may opt only for one of the above options. Selected option needs to be consistently applied to all intercompany loans.

Prescribed interest rates should be applied to interest income/expense recognized during 2018 regardless of the period from which loan(s) originate.

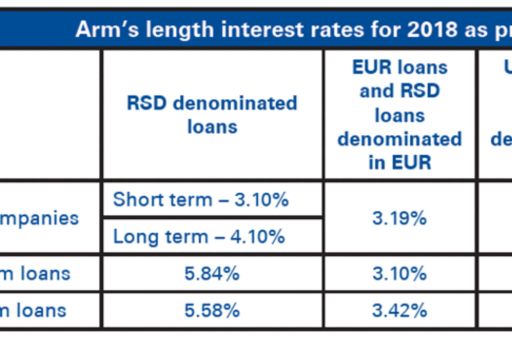

The Rulebook prescribes separate interest rates for long-term and for short-term borrowings for all non-finance entities and a single interest rate for banks and finance leasing companies (except for RSD denominated loans).

In determining the amount of interest which is subject to beneficiary rates prescribed by the applicable Double Tax Treaty (“DTT“), taxpayers may also use prescribed rates or apply general OECD based methods. Unlike to the calculation of transfer pricing adjustments, taxpayers may apply prescribed rates and general methodology interchangeably in determining potential withholding tax exposure.

Arm’s length interest rates for 2018 as prescribed by the MF

What impact this may have on your business?

Slight decreasing trend of interest rates when compared to 2017 is present, except financing in CHF. It is necessary to review if new interest rates for 2018 are aligned with interest rates currently used in your related party financial instruments. In addition, companies exposed to significant / long-term related party financing should consider applying general OECD based methods for assessment of arm’s length interest as prescribed by the CIT Law, as such approach may be more beneficial and provide increased level of certainty in relation to future tax treatment.

If you have any questions or you need assistance of our tax professionals, please contact us at tax@kpmg.rs

KPMG will continue to monitor all relevant developments in this complex area, and inform you about possible impact of these events on business operations.

For previous editions of KPMG Tax Alerts please visit the following web page: KPMG Tax Alerts

We remain at your disposal for any additional information you may require.

KPMG Tax & Legal Department

KPMG d.o.o. Beograd

Kraljice Natalije 11

Belgrade, Serbia

Office: +381 11 20 50 500

© 2024 KPMG d.o.o. Beograd, a Serbian limited liability company and a member firm of the KPMG global organization of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved.

For more detail about the structure of the KPMG global organization please visit https://kpmg.com/governance.