Differences between GAPSME and GAPSE regulations - Part 3

Differences between GAPSME and GAPSE regulations.

Differences between GAPSME and GAPSE regulations.

This article was written by Clifford Delia and Michelle Spiteri Bailey and was published on The Accountant.

This is the third in a series of articles outlining the main differences between General Accounting Principles for Smaller Entities (GAPSE) and General Accounting Principles for Small and Medium-Sized Entities (GAPSME) regulations in relation to its scope, applicability, presentation of financial statements and specific accounting and disclosure requirements. Part three will focus on the requirements of Section nine of GAPSME which deals with financial assets, financial liabilities and equity.

Financial assets, financial liabilities and equity

Whereas one can generally comment that the changes in recognition and measurement requirements for most balance sheet items brought about by GAPSME when compared with GAPSE were quite minimal, this is not the case when it comes to financial assets and liabilities. Section nine of GAPSME was completely rewritten and the recognition and measurement principles of the new regulations bear closer comparison to IAS39 – Financial instruments: recognition and measurement, than to GAPSE.

Under Sections nine and 18 of GAPSE one had the option of measuring certain types of financial instruments at fair value (FV) or at amortised cost, although cost accounting was always an option for all types of financial assets and liabilities. This is no longer the case under GAPSME because the new regulations saw the introduction of a number of categories of financial instruments, and the basis of subsequent measurement depends on the classification of the particular instrument.

Classification of financial instruments

In a similar manner to IAS 39, GAPSME classified financial instruments in the following four categories:

- Financial instruments held for trading

- Held-to-maturity investments

- Loans and receivables

- Available-for-sale financial assets

A financial asset or financial liability is classified as held for trading if:

- it is acquired or incurred principally for selling or repurchasing in the near termon initial recognition

- it is part of a portfolio of identified financial instruments that are managed together and for which there is evidence of a recent pattern of short-term profit-taking

- it is a derivative (except for a derivative that is a designated and effective hedging instrument).

Held-to-maturity investments are non derivative financial assets with fixed or determinable payments and fixed maturity that an entity has the positive intention and ability to hold to maturity other than those designated as other than investments designated as available-for-sale or as loans and receivables.

GAPSME features a tainting provision that prohibits an entity from classifying any financial assets as held to maturity if the entity has, during the current financial year or during the two preceding financial years, sold or reclassified more than an insignificant amount of held-to-maturity investments before maturity. The regulation provides for three particular instances where the tainting provision does not come into play, such as when the premature sale happened as a result of an isolated event that was beyond the entity’s control, is nonrecurring and could not have been reasonably anticipated by the entity.

Loans and receivables are non derivative financial assets with fixed or determinable payments that are not quoted in an active market, other than those classified as held for trading or as available-for-sale.

Available-for-sale financial assets are those non-derivative financial assets that are designated as available-for-sale or are not classified as loans and receivables, held-to-maturity investments or held for trading financial assets.

Initial recognition and measurement

Under both GAPSE and GAPSME regulations, an entity shall recognise a financial asset or a financial liability in its balance sheet when the entity becomes a party to the contractual provisions of the instrument.

As for initial measurement, under GAPSE, upon initial recognition, financial assets and liabilities were measured at cost (purchase price plus transaction costs). This is no longer the case under the new regulations which require financial assets and liabilities to be initially measured at FV (and not at face or nominal value). For financial assets or liabilities not classified as held for trading, initial measurement should be at fair value plus transaction costs. Transaction costs must be directly attributable to the acquisition or issue of the financial asset or financial liability.

Subsequent Measurement

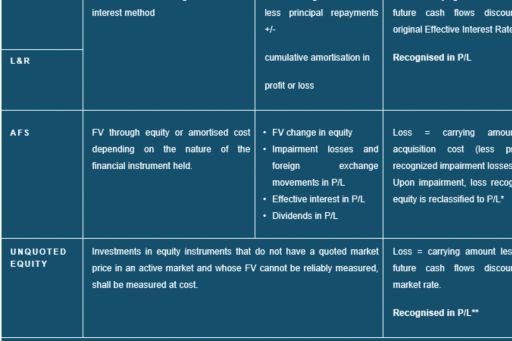

Under GAPSE, quoted and held for trading investments were measured at cost less impairment or at fair value. Unquoted investments were measured at cost and for other types of long term loans and investments at amortised cost was encouraged but not mandatory.

Under GAPSME, subsequent measurement rules for the different classes of financial instruments are as follows:

GAPSME gives additional guidance on GAPSE on how FV is calculated

FV is defined as the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm’s length transaction.

The best evidence of FV is quoted prices in an active market. If the market for a financial instrument is not active, an entity establishes FV by using a valuation technique. Valuation techniques include using recent arm’s length market transactions between knowledgeable, willing parties, if available, reference to the current FV of another instrument that is substantially the same, discounted cash flow analysis and other models. If there is a valuation technique commonly used by market participants to price the instrument and that technique has been demonstrated to provide reliable estimates of prices obtained in actual market transactions, the entity should use that technique.

Periodically, an entity should calibrate the valuation technique and tests it for validity, using prices from any observable current market transactions in the same instrument or based on any available observable market data.

Hedging Whereas GAPSE was silent about hedging, GAPSME recognises three different types of hedging relationships: FV hedges, cash flow hedges and hedges of a net investment in a foreign operation. A hedging relationship qualifies for hedge accounting if a number of conditions as specified in section 9.32 of the GAPSME regulations are met.

Gains or losses from the hedging instrument and the hedged item of a FV hedge are recognized in profit or loss. The effective portion of gains or losses from the hedging instrument of a cash flow hedge are recognised directly in equity and the gains or losses of the ineffective portion of a cash flow hedge are recognized in profit or loss. Gains or losses on hedges of a net investment in a foreign operation are accounted for similarly to cash flow hedges.

Disclosures for all entities

For financial instruments measured at FV an entity shall disclose the following, for each category of financial instrument:

- Significant assumptions underlying the valuation models and techniques used

- FV at the balance sheet date and the changes in FV recognized

- Accounting policy for each category of financial instrument

- Detailed reconciliation of the carrying amount of each category of instrument or investment, classified as non-current assets at the beginning and end of the period

- Table showing movements in FV reserves during the financial year

For each class of derivative financial instrument, an entity shall disclose in the notes, information about the extent and the nature of the instruments, including significant terms and conditions that may affect the amount, timing and certainty of future cash flows.

For financial liabilities, an entity shall disclose:

- Amounts owed by the entity becoming due and payable after more than five years

- Financial liabilities covered by a valuable security furnished by the entity, together with an indication of the nature and form of the security given

Equity disclosures

All equity disclosures required by GAPSE (Section 18.22) are no longer required for small entities under the new regulations. However, medium sized entities are still required to present disclosures such as: the number of authorised and issued shares; nominal and par value of shares; rights, preferences and restriction on each class of shares; details on purpose of reserves; existence of any convertible debentures, warrants, options or similar securities and their rights; details on redemption options; dividends paid; dividends declared but still due at end of reporting period; dividends proposed after end of reporting period; and own shares held by entity itself.

Additional disclosures for medium-sized entities

A medium-sized entity shall also disclose:

- The market value of quoted investments carried at cost or amortised cost if it is materially different from their carrying amount

- For unquoted non current investments which are carried at cost or amortised cost and have a carrying amount that is higher than their FV disclose

- the book value and the FV of either the individual assets or appropriate groupings of those individual assets

- the reasons for not reducing the book value, including the nature of the evidence underlying the assumption that the book value will be recovered

- If an investment is carried at cost because FV cannot be measured reliably, this fact is to be disclosed together with reasons why FV cannot be measured reliably

- Disclose the financial assets that the entity has pledged as collateral for liabilities or contingent liabilities

Conclusion

This article gives a few details of the new GAPSME regulations with particular emphasis on the changes in measurement and disclosure requirements for financial instruments which merit to be highlighted.

The article in the next issue will continue the analysis of the different line items describing changes between GAPSE and GAPSME, focusing related party disclosures, business combinations and goodwill, and consolidated financial statements.

This article is not intended to be a comprehensive review of the new GAPSME regulations, but the scope is to focus on a number of salient points emanating from the change from GAPSE to GAPSME regulations. Readers are advised to refer to the full regulations included in subsidiary legislation S.L.281.05 Accountancy Profession (General Accounting Principles for Small- and medium-sized entities) regulations

© 2024 KPMG, a Maltese civil partnership and a member firm of the KPMG global organisation of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved.

For more detail about the structure of the KPMG global organization please visit https://kpmg.com/governance.