iGaming – Numbers not for punters only

iGaming – Numbers not for punters only

Malta has indisputably become synonymous with the iGaming industry and today proudly presents itself as a gaming hub.

Malta has indisputably become synonymous with the iGaming industry and today proudly presents itself as a gaming hub. Over the course of the last twelve years, the industry has become a fundamental part of our economic structure. Industry stakeholders estimate that the sector today contributes around 10–12% to Malta’s overall GDP forming part of a wider boom. Global and European demand for remote gaming products and services remains on a strong growth trajectory across market and product ranges. In fact, the European market for remote gaming is currently the largest market in the world. 47.6% per cent of the €34.6bn of online gaming gross win (stakes minus winnings) originated from the EU market itself. Research projects that the European online gambling’s Gross Gaming Revenue is expected to rise from €16.5 billion in 2015 to €24.9 billion in 2020. Industry players and decision makers understand its significance to the economy as a whole, resulting in a strong commitment to this sector (EGBA, 2016)i.

Malta has been able to capitalise on its EU first mover advantage, and has continued to be proactive in developing its regulatory framework to sustain the island’s competitive edge at the forefront of the gaming sphere. Today, Malta hosts in excess of 280 remote iGaming operators holding 460 plus active licences (Mifsud)ii for online offerings such as casino-type games, online lotteries, poker derivative games, peer-to-peer (P2P) gaming and game portals, and sports book operators, amongst others. As expected, such iGaming operators have incorporated limited liability companies in Malta and akin to other businesses, have an obligation to report their results to their shareholders. As many accountants in public practice involved in the iGaming sector will agree, the process of preparing such financial statements offers a challenge on a number of fronts. The purpose of this article is to explore some of the more challenging aspects that we believe will arise from the preparatory groundwork of such financial statements, once new accounting standards on revenue and leases come into force.

REVENUE RECOGNITION in terms of IFRS 15

As with any iGaming operation, one area of focus which elicits interest - not only from a pure business perspective but also from an accounting point of view - is revenue recognition. The extent of complexity to account for revenue with such operators depends very much on the type of transactions entered into with punters.

As we approach the end of 2016, the effective date of the new revenue standard IFRS 15 is fast approaching. Entities will have to adopt IFRS 15 for financial reporting periods beginning on or after 1 January 2018, subject to endorsement by the EU, which the European Financial Reporting Advisory Group (EFRAG) expects to be forthcoming before the standard’s effective date (EFRAG, 2016)iii.

Given the underlying complexity of certain transactions entered into by iGaming operators, coupled with the novelty of IFRS 15, it is certainly opportune to grasp a good understanding of how the accounting for iGaming revenue will be affected upon the adoption of IFRS 15. Such a detailed exercise is certainly beyond the scope of this article, nevertheless below we highlight some of the relevant considerations.

The first step in the new revenue recognition step plan requires an entity to identify the contract with a customer. A contract with a customer is in the scope of the new standard when the contract is legally enforceable and certain other criteria set out in the standard are met. By virtue of customer placing and acceptance by the relevant entity of a wager, both parties have approved the transaction and are aware of the underlying rights and obligations.

Specifically of relevance to this first step is the fact that, the gaming (wagering) transaction represents the contract between the customer (the punter) and the gaming entity. Such contract bestows rights and obligations upon both parties, whereby, based on the outcome of an event (such as the results of accumulated cards in a hand of play for a table game or the result of a match) either of the following outcomes is possible:

(a) the gaming entity retains the amount wagered by the customer, or

(b) the wager is returned to the customer along with an additional amount effectively representing the gaming entity’s side of the wager in the agreement.

Therefore, a wagering transaction may result in a net inflow or a net outflow of consideration for the gaming entity.

Scope is key! While an iGaming operator may enter into different transactions with punters depending on the type of product offering, these can be broadly split up into two categories:

a. Transactions in which the iGaming operator administers a scheme among its punters and receives a commission based on the amount wagered. In such transactions, the iGaming operator will receive its commission regardless of the outcome of the wager;

b. Transactions in which the iGaming operator takes a position against the punter. In such a scenario, the value of the individual contract is contingent upon the outcome of a specified event and the iGaming operator is not, therefore, normally guaranteed a specific commission or return.

In the second step of the new standard’s revenue recognition model, an entity identifies the performance obligations of the contract with the customer. The process of identifying performance obligations requires an entity to determine whether it promises to transfer either goods or services that are distinct, or a series of distinct goods or services that meet certain conditions. For example, on a Blackjack table, two elements of the obligation – that is honouring the outcome of the hand of play and making the appropriate pay-out – are not separable and therefore, constitute one performance obligation.

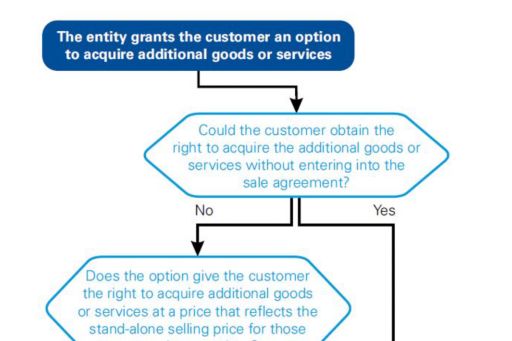

Determining whether a customer has been given an option to acquire additional goods and services under loyalty programmes, which is common practice in the iGaming sector, and the accounting for such an option are also relevant.

The following flow chart helps analyse whether a customer option is a performance obligation:

Next, an entity determines the transaction price. The transaction price is the amount to which the entity expects to be entitled in exchange for the transfer of goods and services. When making this determination, the iGaming entity will consider past customary business practices. If the contract contains elements of variable consideration (such as refunds and incentives) then these have to be considered as well. The standard also addresses the uncertainty relation to the latter type of consideration and limits the amount of such consideration that can be recognised – which in a nutshell involves recognising variable consideration in the transaction price, if, and to the extent that its inclusion will not result in a significant revenue reversal in the future when the uncertainty has been subsequently resolved.

The transaction price is measured as the difference between gaming wins and losses, as opposed to the total amount wagered. This is commonly referred to as “win” or “gross gaming revenue”.

The above step is followed by a fourth step which involves the allocation of the price to the separate performance obligations on the basis of their standalone selling prices. The transaction price in a wagering transaction is therefore the amount of consideration to which a gaming entity expects to be entitled in exchange for transferring promised goods or services to a customer. Based on statistical probabilities, a gaming entity would expect to realise a net win (or net consideration) from the aggregation of all the individual gaming transactions with a customer, over a relationship period. A net loss over such a relationship period is expected to be infrequent or rare. Nevertheless, the transaction price in a wagering transaction may be negative due to the consideration payable to the customer in the transaction as a result of the customer winning the wager.

Finally, as a fifth step, IFRS 15 provides for two revenue recognition patterns – over time, or at a point in time. The application of either is not a matter of choice, but is driven by the satisfaction of the performance obligation. For example, in a hand of Blackjack, the performance obligation (i.e. honouring the outcome of the hand of play and making the appropriate pay-out) is satisfied and the revenue recognised at a point in time that is within a few minutes of the placement of the bet by the customer. However, in a sports betting transaction, the performance obligation may be satisfied at a later date, possibly in a subsequent financial reporting period which is tied to the occurrence of the event to which the betting transaction relates.

THE NEW LEASES STANDARD

Another standard coming into force over the next few years is IFRS 16 - the new leases standard.

IFRS 16 Leases is effective for financial reporting periods beginning on or after 1 January 2019, with earlier application permitted only if IFRS 15 Revenue from Contracts with Customers is also applied.

The new standard removes the concept of operating and finance leases for lessees and replaces it with a single accounting model under which lessees must recognise all significant leases on balance sheet.

While licences of intellectual property granted by a lessor within the scope of IFRS 15 Revenue from Contracts with Customers - such as licences conveying the right to use gaming platforms under white label agreements which will remain out of scope of the leases standard - gaming entities will have to consider the applicability of IFRS 16 to leases of various other assets such as property used to run the iGaming operations.

The accounting change is not limited to the balance sheet. Amongst other ongoing impacts, the lease expense profile will be front-loaded for most leases, even when rental payments are constant year-to-year. New information will also be required to support the determination of new judgements and estimates.

Key financial metrics will be affected by the new accounting model, which will change KPIs and introduce P&L and balance sheet volatility.

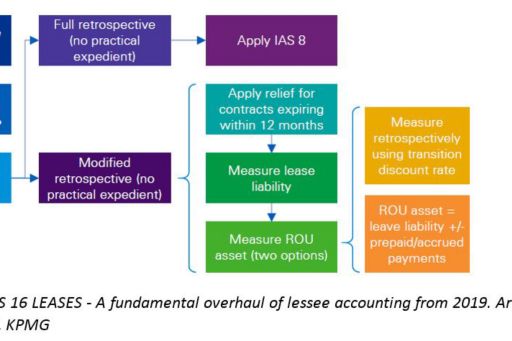

Luckily, on transition to IFRS 16, an entity will have a number of interdependent options and practical expedients available. Selecting different options will result in a different impact on transition and also prospectively in the periods following the adoption of the standard. The below flowchart illustrates a simplified view of the transition options available under the standard.

As IFRS 16 Leases changed the definition of a lease and shifted its focus on which party controls the use of an asset, many iGaming operators will have to re-evaluate the various arrangements they already have in place to determine if they are leases under the new standard, as those that do meet the definition would, under the new standard, be required to be recognised on the balance sheet.

The accounting by the lessee will be done by recognising, at inception of the lease, a right of use (ROU) asset on the balance sheet which will show that the lessee has the right to use that particular asset.

The lessee will also have to recognise, at inception of the lease, a lease liability which represents the obligation to pay future lease payments to the lessor. Such lease liability, at inception of the lease, will include the present value of lease rentals and the present value of expected payments at the end of the lease. This includes cash flows arising from any fixed payments expected to be incurred by the lessee over the lease term, any variable lease payments, payments that would be incurred by the lessee to exercise a purchase option having a significant economic incentive, residual value guarantees payments, and termination option penalties.

Initially, the ROU asset is recognised by the lessee in the balance sheet at the value of the lease liability plus any initial direct costs, any prepaid lease expenses and any estimated costs to dismantle, remove or restore the underlying asset. The ROU asset is subsequently amortised and tested for impairment under the applicable standard.

On the other hand, the liability is subsequently measured by the amortised cost method using the effective interest method.

The main impact on the balance sheet of the lessees having operating leases, resulting from the new standard, will be that they will appear to have more assets, but they will also appear to have more debt. An impact on the income statement will also arise due to the fact that the total lease expense will be front loaded, even if the cash payments are constant. The fact that under the current standard, certain lessees have nothing recognised in their balance sheet, will have an effect on the key financial metrics, such as key performance indicators of the lessee. Various key performance indicators such as return on assets, return on capital, asset turnover, debt-to-asset ratio, debt-to-equity ratio, interest cover ratio and earnings before interest, depreciation, tax and amortisation (EBIDTA) will be effected because the lessee will now have to recognise the lease on the balance sheet.

WHAT DOES THE FUTURE HOLD?

In the past within the iGaming sector there has certainly been discussion over how an iGaming entity should account for bets or wagers receivediv and over certain other areas such as the accounting for jackpots and bonuses. However, as the sector continues to develop, there are and will continue to be other challenges with regards to the accounting aspects that need to be considered. Presently, looming on the horizon are the new accounting standards IFRS 15 on Revenue from Contracts with Customers - which as we have seen establishes a comprehensive framework for determining whether, how much and when revenue is recognised and which replaces the other accounting standards dealing with this area such as IAS 18 Revenue and IFRIC 13 Customer Loyalty Programmes. The other accounting aspect which is and continues to gain momentum is certainly that related to the new accounting standard on leases and accountants in public practice involved in the iGaming sector will for sure need to think and plan ahead in order to ensure a smooth transition once these accounting standards come into force.

______________________

iEuropean Gaming and Betting Association (EGBA) (2016), Facts and Figures – Market Reality, available on egba.eu.

iiMifsud, R. (2016), Business Opportunities in the Mergers and Acquisitions Space, Gaming Malta, Ed. 2016, p. 46 – 47

iiiEuropean Financial Reporting Advisory Group (EFRAG) (2016), The EU endorsement status report Position as at 7 October 2016, available on www.efrag.org.

ivINFORMATION FOR OBSERVERS, IFRIC meeting: May 2007, London, Project: Gaming Transactions (Agenda Paper 11(i))

Article as published on The Accountant Autumn 2016 issue.

© 2024 KPMG, a Maltese civil partnership and a member firm of the KPMG global organisation of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved.

For more detail about the structure of the KPMG global organization please visit https://kpmg.com/governance.